Three things about Shanshan. Click the icons for more details.

Science

My research is centered on techniques for scalable and accurate inference in time-varying network structures, statistical modeling of data, large-scale optimization, and robust anomaly detection in time series, and is motivated by a range of applications, in particular ones in bioinformatics and quantitative finance. Checkout my Google scholar profile.

Projects

Many fields and industries are witnessing huge increases in the quantity and complexity of data. This changing data paradigm will only lead to a similarly dramatic increase in theoretical understanding and useful technologies. Creating and applying these statistical and machine learning algorithms is the focus of my research. And I'd like to share methods on Github, where you can find a lot of amazing stuffs.

Communication

If you are interested in machine learning, big data, quantitative finance or any questions about my research, come follow me on twitter. I'd like to have open discussions about these topics 24/7.

Publications

Estimation and detection of network variation in intraday stock market

Journal of Network Theory in Finance

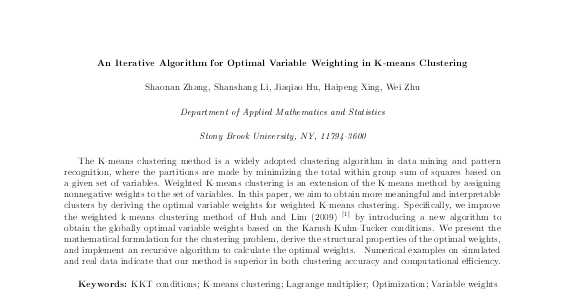

An iterative algorithm for optimal variable weighting in K-means clustering

Communications in Statistics (submitted)

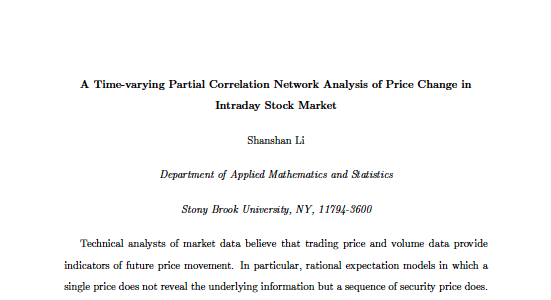

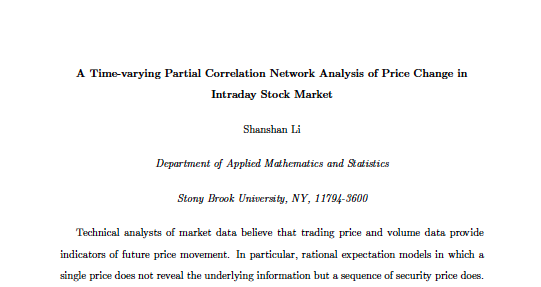

A Time-varying Partial Correlation Network Analysis of Price Change in Intraday Stock Market

News

May 2017

Graduation Hooding Ceremony

Location: Stony Brook, NY

November 2016

Thesis Defense

Title: Estimation and Detection of Network Variation in Intraday Stock Market .

The last few years have witnessed an exponential growth in the collection and analysis of financial market data. Investigating the interactions between the dynamics of the financial system and extracting useful information from these multivariate data streams can help us in improving our understanding of the underlying backbone in the financial market. These massive noisy data sets require the application of suitable and efficient dependency measurements for their analysis in a real-time environment. And that is why network analysis has emerged recently, which is a plausible representation helps interpret the hidden interconnection between the elements in large datasets. However, most frequently used methods in this area have certain limitations, such as the computational complexity or the assumption of a temporally invariant network. This thesis has two major purposes; firstly, to construct time-varying networks by presenting two new approaches to dynamically measure symmetric and asymmetric interactions; and secondly, to detect the structural breaks in the high dimensional time series of the financial market.

The K-means clustering method is a widely adopted clustering algorithm in data mining and pattern recognition, where the partitions are made by minimizing the total within group sum of squares based on a given set of variables. Weighted K-means clustering is an extension of the K-means method by assigning nonnegative weights to the set of variables. In this paper, we aim to obtain more meaningful and interpretable clusters by deriving the optimal variable weights for weighted K-means clustering. Specifically, we improve the weighted k-means clustering method of Huh and Lim (2009) [1] by introducing a new algorithm to obtain the globally optimal variable weights based on the Karush-Kuhn-Tucker conditions. We present the mathematical formulation for the clustering problem, derive the structural properties of the optimal weights, and implement an iteration algorithm to calculate the optimal weights. Numerical examples on simulated and real data indicate that our method is superior in both clustering accuracy and computational efficiency.

Nowadays, giant datasets are collected with lots of empirical information about the functioning of almost every field of study, at a cost much lower than a few decades ago, for instance biotechnology(McBride 2012), medical science(Groves 2013), and in particular business and economics study(Einav and Levin 2013). One can be interested in the existing linkages between the different elements that included in a collection of the dataset. And that is the reason why Network Analysis has emerged in recent years. Network Analysis is used to help interpret the hidden interconnections between different elements in large dataset. With the application of proper statistical tools, analysts can not only get the statistical results about the data, but also plot the interconnections of large multivariate time series system in a graphical representation that eases the interpretation of the real market observation. That is to say, Network Analysis allow us to construct graphs representing the reality behind those complex empirical datasets.